Strait of Hormuz Disruption and the New Geopolitics of Energy Flows

HIIA Perspective – Written by Máté Kováts

On February 28, the United States and Israel started a joint military attack against Iran, first targeting its military bases and naval forces. The attack aimed to prevent Iran from developing nuclear weapons and to replace the long-standing Iranian leadership, which was responsible for destabilization in the Middle East. Although the main focus is currently on military actions within Iran, there is one other issue that could affect not just Iran or the Middle East, but the whole world. This is the flow of energy, and the halt of that around the Arabian Peninsula.

Even before the military action started, several sources already highlighted how Iran could disturb the global flow of energy in response to an attack on the country. Since Tehran has significant influence over the Strait of Hormuz, the Iranian leadership was expected to make attempts at closing the strait and, by doing so, pressure regional actors like Qatar, Saudi Arabia, and the United Arab Emirates. By March 1, sources confirmed that Iran had managed to close the Strait of Hormuz, halting trade through the Persian Gulf. Approximately 20 percent of the global flow of oil passed through the currently closed strait,[1] which is so significant that it could create real chaos on oil markets, which opened on March 2.

The current situation is not only concerning because Iran has lost its ability to sell oil, but also, more importantly, because other significant regional actors have halted their own exports. The new situation will most likely affect not only the Middle Eastern countries, but also several other states, such as China and European Union members. At the same time, several Iranian missiles damaged energy infrastructure in the region. Qatar halted LNG and related output after Iranian strikes targeted the country’s main LNG export hub in Ras Laffan.[2] Besides Qatar, multiple other countries’ energy infrastructure was targeted in the past couple of days, including that of the United Arab Emirates,[3] Oman,[4] and Kuwait.[5]

The PDF version is available here!

Iran’s Position as a Global Energy Supplier

Iran has the third largest proven crude oil reserves in the world,[6] which makes Tehran a significant global actor when it comes to energy and energy export. However, for decades Iran’s oil exports have been constrained by U.S. sanctions, which notably tightened in 1995. The most direct global export choke points emerged in 2011–2012[7] via restrictions on Iran’s central bank and oil exports and the 2012 EU oil embargo.[8] These were then re-intensified with the U.S. reimposition of petroleum sanctions in November 2018.[9] This situation decreases Iran’s importance in the global oil market; still, Iran managed to export oil to important global actors, such as China. Lately, Iranian crude oil represented approximately 12–15 percent of China’s seaborne oil imports.[10] Since China is the largest oil-importing country in the world, a possible halt of these exports to Beijing could cause significant damage to China’s economy and industry sector. Iran’s main oil-exporting terminal is Kharg Island,[11] which is located in the northern part of the Persian Gulf, next to Iran’s western border. Due to the current halt in shipments leaving or entering the Persian Gulf, Iran is also unable to deliver its oil to its trading partners.

Tehran has several options to disrupt shipments and close the Strait. One of these options is to fire missiles at passing ships. This option is rather theoretical so far, since a sunk ship could close the strait for much longer than it would be in the interest of Tehran. Another, more rational option is for Iran to deploy sea mines to prevent any ships from even trying to cross the strait. The advantage of this option would be that Tehran may not actually need to deploy mines; it may be enough to announce the move and pretend it was made, which would force shipping companies to order their ships to stay in ports in the Persian Gulf. Since March 1, the Iranian regime managed to partly close the Strait of Hormuz and stop the majority of ships from entering or leaving the Persian Gulf. By doing so, Iran managed to prevent shipments from Iraq, Kuwait, Saudi Arabia, and the United Arab Emirates, among others. By halting these exports, Iran affects not only the region and China, but also almost every other region in the world.

What Could Happen to Oil Prices?

Many compare the current conflict to the Twelve-Day War in 2025 and suggest that this will also end with a quick sell-off[12] on the oil market. Currently, it looks like history will not repeat itself in this case. The new military conflict between Iran, Israel, and the United States is expected to last longer than before, which could result in a different market reaction. At noon on March 1, OPEC+ countries had an emergency meeting online, where the member states agreed to increase oil production to counterbalance the expected market reactions to the war.[13]

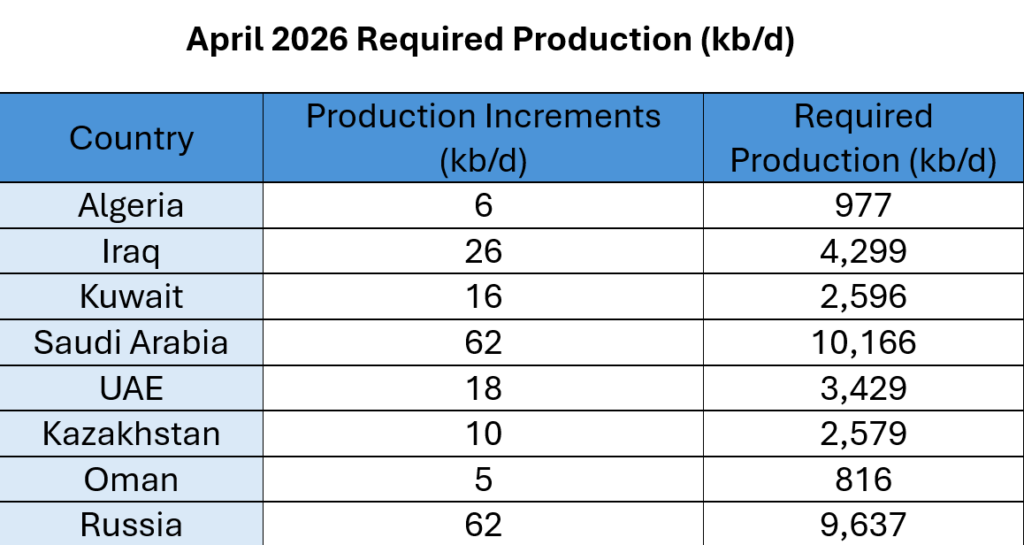

Figure 1. April 2026 Required Production. Source: OPEC.[14]

Although the member states agreed only to increase oil production by 206 thousand barrels per day (kb/d),[15] this is likely because markets only reopened on March 2, and member states had no clear sign whether crude oil prices would go up by only 3 percent or 15 percent. Still, the fact that OPEC+ had to make a quick adjustment shows that they expect the effects of the war to last longer and influence the market more than during the Twelve-Day War or other previous cases. The role of Saudi Arabia and Russia can be significant in market stabilization, since these two states are the only swing countries able to make rapid, high-volume changes in their oil production—either cuts or increases—without major economic suffering. This is due to their crude oil reserves and economic systems, which are prepared for such outstanding scenarios. Still, given the fact that the Strait of Hormuz was closed after the military action started, Saudi Arabia’s power at the moment is questionable, since even if it is able to suddenly increase production, the problem of exportation is still not solved, which will not decrease the market’s uncertainty for the moment.

By March 3, the Brent oil price jumped from $72 per barrel on February 27 to $80–82 per barrel due to market instability. This signals that the OPEC+ announcement calmed the market a bit, since previous predictions suggested prices this week would hit around $100 per barrel, but the significant jump still shows the seriousness of the developments.

Possible Effects on the European Union

Even if the European Union is not reliant on Iranian oil exports, the global market shifts can still hurt the Union’s member states. The global price of oil will have effects beyond the Middle East, and since the EU is relying heavily on energy imports,[16] changes will most likely affect these imports too. The uncertainty in the global oil market will result in higher crude and refined oil product prices, with a possible increase in importation costs. If the prices go too high, they could put inflation pressure on the European Union,[17] which in the long term could result in weaker industrial competitiveness,[18] an issue that the EU has already been suffering from since energy prices rose following the first sanctions on Russian energy.[19] Member states must take into account the fact that the longer these oil exports stay halted at the Strait of Hormuz, the higher the prices of refined oil products will be.

Also, since the current war affects not only oil exports but also trading routes for seaborne LNG, the EU could easily fall into a bidding war with Asia on the flexible seaborne cargoes.[20] If the trading routes stay disturbed, the European Union will have to make a decision on whether to accept paying higher prices for the imported LNG or see higher volatility in the volume of imports.

Lastly, the European Union must take into account the increased risks that shipping companies are taking by delivering anything along the coast of the Arabian Peninsula. Based on the Financial Times’ information,[21] the rise in insurance prices could reach even 50 percent in the coming days. This would mean that the European Union would have to face higher delivery costs, possible delays, and scheduling uncertainty. Philip R. Lane, a member of the ECB’s Executive Board, highlighted that an increase in oil and gas prices will have a direct influence on EU member states’ economies, and they expect a rise in inflation by at least 0.5 percent,[22] but this could be even higher based on the length of the conflict. On March 2, the Dutch TTF front-month[23] already rose by 50 percent,[24] signaling the upcoming effect of the Iranian war on the European energy sector.

Conclusion

The future is hard to predict, since multiple indicators are influencing the outcome at the same time. The most interesting question—and the most important one for the European energy sector—is how long the Strait of Hormuz will be closed by Iran. If the disruption at the strait ends in the coming days, Europe will most likely face only limited economic effects and lower inflation waves. However, if the Strait stays closed for a longer period—weeks or even months—the European Union will face significant economic challenges, with higher energy prices and higher inflation. At the same time, if the Houthis start to attack ships in the Red Sea as a sign of support for Iran, that could further escalate the destabilization of the energy market, with a possible result being an even more drastic increase in European energy prices.

The war between Iran and the United States and Israel has become a global energy security event not primarily because of the immediate loss of Iranian barrels, but because it has triggered a deliverability crisis in the world’s most sensitive hydrocarbon corridor. The closure of the Strait of Hormuz transforms a regional military escalation into a systemic market shock: It constrains exports from multiple Gulf producers at the same time, increases insurance and delivery costs, and injects a durable geopolitical risk premium into crude and refined product prices. In this setting, market outcomes will be driven less by announced production levels and more by the credibility of physical delivery, whether energy can be loaded, insured, and shipped safely. For the European Union, the conflict is a test of economic resilience and energy-market flexibility rather than direct dependence on Iranian supply. Europe will most likely absorb the shock through global benchmark pricing, potential tightening in refined product markets, and—perhaps most critically—through LNG competition if Asian buyers bid aggressively for flexible cargoes. In parallel, disruptions in maritime logistics can raise delivered costs and introduce delays across energy and non-energy trade alike, turning a distant conflict into a competitiveness challenge at home.

Endnotes

[1] Candace Dunn and Justine Barden, “Amid Regional Conflict, the Strait of Hormuz Remains Critical Oil Chokepoint,” U.S. Energy Information Agency, June 16, 2025, https://www.eia.gov/todayinenergy/detail.php?id=65504.

[2] Marwa Rashad, “Qatar’s Role in the Global Gas Market,” Reuters, March 2, 2026, https://www.reuters.com/business/energy/qatars-role-global-gas-market-2026-03-02/.

[3] “Drone Attack Targets UAE’s Musaffah Fuel Tank Terminal, No Impact on Operations,” Reuters, March 2, 2026, https://www.reuters.com/world/middle-east/drone-attack-targets-uaes-musaffah-fuel-tank-terminal-no-impact-operations-2026-03-02/.

[4] “Drone Hits Fuel Tank at Oman’s Duqm Port,” Reuters, March 3, 2026, https://www.reuters.com/world/middle-east/drone-hits-fuel-tank-omans-duqm-port-2026-03-03/.

[5] “Several US Military Aircraft Crash in Kuwait as Iranian Strikes Continue,” The Kathmandu Post, March 2, 2026, https://kathmandupost.com/world/2026/03/02/several-us-military-aircraft-crash-in-kuwait-as-iranian-strikes-continue.

[6] “Annual Statistical Bulletin,” Organization of the Petroleum Exporting Countries, accessed March 1, 2026, https://www.opec.org/annual-statistical-bulletin.html.

[7] “Fact Sheet: Sanctions Related to Iran,” The White House, July 31, 2012, https://obamawhitehouse.archives.gov/the-press-office/2012/07/31/fact-sheet-sanctions-related-iran.

[8] Council of the European Union, “Council Decision 2012/35/CFSP of January 23, 2012, Amending Decision 2010/413/CFSP Concerning Restrictive Measures against Iran,” Official Journal of the European Union L 19 (January 24, 2012): 22–30, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32012D0035.

[9] “Re-Imposition of the Sanctions on Iran That Had Been Lifted or Waived under the JCPOA,” U.S. Department of the Treasury Office of Foreign Assets Control, November 4, 2018, https://ofac.treasury.gov/sanctions-programs-and-country-information/iran-sanctions/re-imposition-of-the-sanctions-on-iran-that-had-been-lifted-or-waived-under-the-jcpoa.

[10] “China’s Heavy Reliance on Iranian Oil Imports,” Reuters, January 13, 2026, https://www.reuters.com/business/energy/chinas-heavy-reliance-iranian-oil-imports-2026-01-13.

[11] Malcolm Moore et al., “How Will Strikes on Iran Affect Global Energy Flows?,” Financial Times, February 28, 2026, https://www.ft.com/content/baa400cc-359c-4205-b93d-573b5b7c440d.

[12] Sell-off is a rapid wave of selling in a market that pushes prices down sharply, often because traders reevaluate expectations of the issue that affected prices at the market.

[13] “Saudi Arabia, Russia, Iraq, UAE, Kuwait, Kazakhstan, Algeria, and Oman Adjust Production and Reaffirm Commitment to Market Stability,” Organization of the Petroleum Exporting Countries, March 1, 2026, https://www.opec.org/pr-detail/1619593-1-march-2026.html.

[14] “Saudi Arabia, Russia, Iraq, UAE, Kuwait, Kazakhstan, Algeria, and Oman Adjust Production.”

[15] “Saudi Arabia, Russia, Iraq, UAE, Kuwait, Kazakhstan, Algeria, and Oman Adjust Production.”

[16] “Energy Statistics – An Overview,” Eurostat, accessed March 1, 2026, https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Energy_statistics_-_an_overview.

[17] Chikako Baba and Jaewoo Lee, “Second-Round Effects of Oil Price Shocks — Implications for Europe’s Inflation Outlook,” International Monetary Fund, September 9, 2022, https://www.imf.org/en/publications/wp/issues/2022/09/06/second-round-effects-of-oil-price-shocks-implications-for-europes-inflation-outlook-523201.

[18] Julien Le Roux et al., “How Higher Oil Prices Could Affect Euro Area Potential Output,” European Central Bank, August 1, 2022, https://www.ecb.europa.eu/press/economic-bulletin/focus/2022/html/ecb.ebbox202205_04~f296647c4b.en.html.

[19] Ruslan Bortnik and Máté Kováts, “How Europe Lost Competitiveness: The Hard Fate of a Hostage to Geopolitics,” Hungarian Institute of International Affairs, February 26, 2026, https://hiia.hu/en/how-europe-lost-competitiveness-the-hard-fate-of-a-hostage-to-geopolitics/.

[20] “Gas 2025 – Analysis,” International Energy Agency, October 27, 2025, https://www.iea.org/reports/gas-2025.

[21] Jamie John et al., “Insurers to Cancel Policies and Raise Prices for Ships in Gulf and Strait of Hormuz,” Financial Times, February 28, 2026, https://www.ft.com/content/2dc114d0-5bb3-4fae-b538-9a050954549a.

[22] European Central Bank, “Interview with Philip R. Lane, Member of the Executive Board of the ECB, conducted by Olaf Storbeck on 26 February 2026,” March 3, 2026, https://www.ecb.europa.eu/press/inter/date/2026/html/ecb.in260303~768fa10188.en.html.

[23] The Dutch TTF is the main European wholesale gas benchmark.

[24] Kate Abnett, “EU Calls Gas Supply Group Meeting in Response to Iran Conflict,” Reuters, March 2, 2026, https://www.reuters.com/business/energy/eu-policymakers-expect-no-immediate-oil-security-impact-iran-conflict-email-2026-03-02/.